Source: https://www.iras.gov.sg/taxes/stamp-duty/for-property/buying-or-acquiring-property/buyer’s-stamp-duty-(bsd)

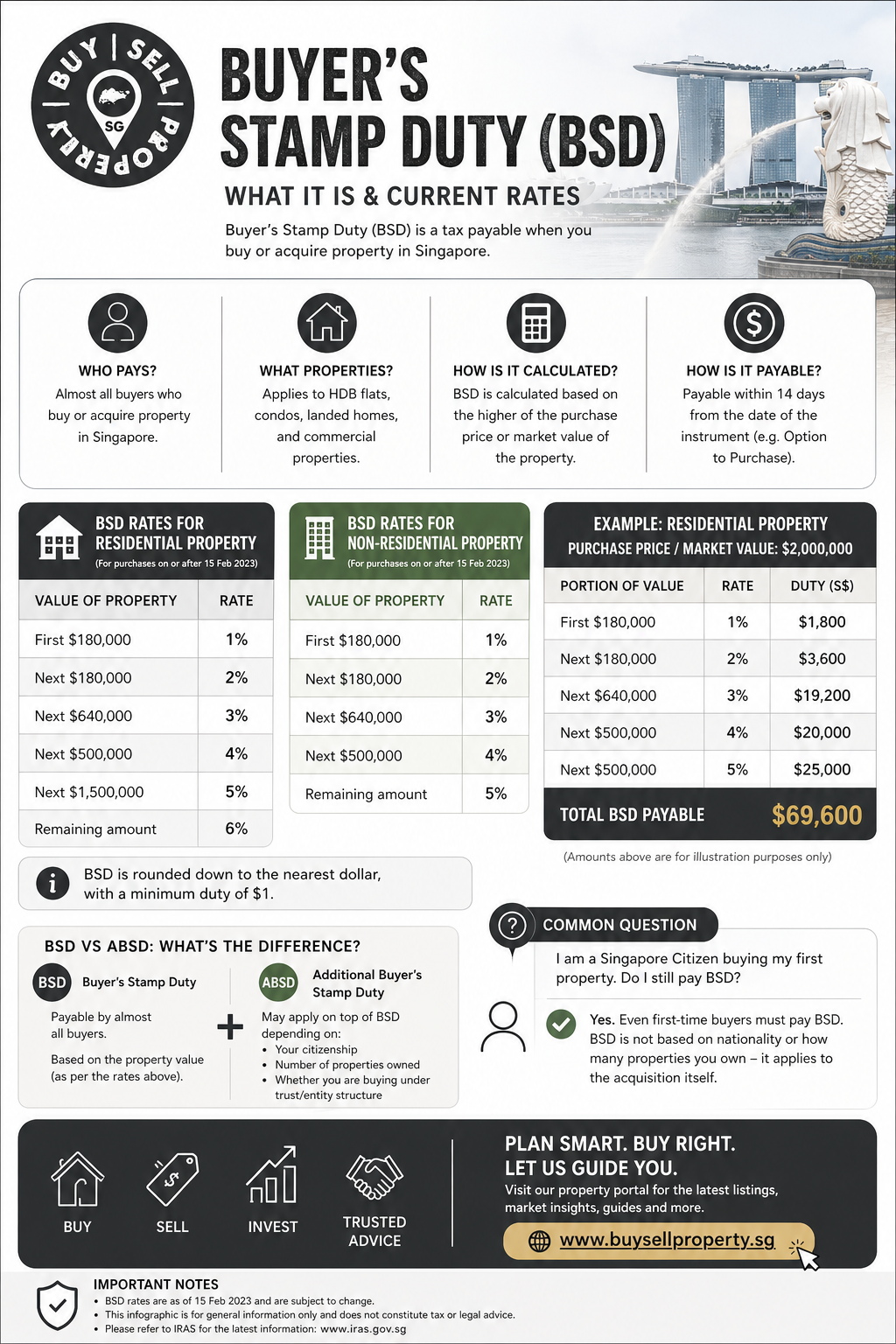

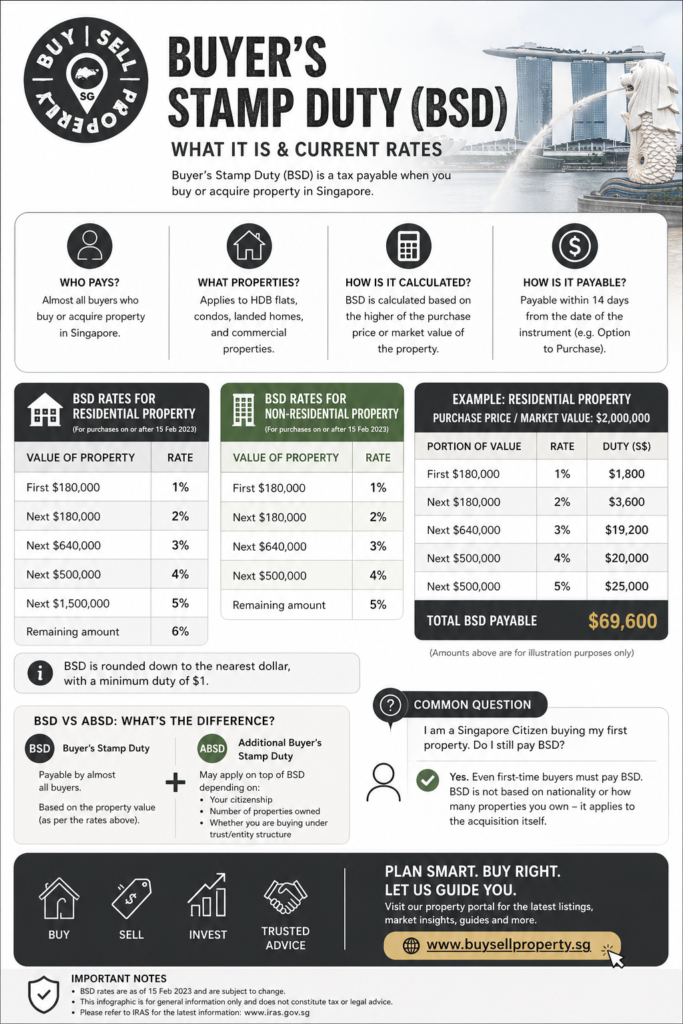

You are required to pay BSD for documents executed for the transfer or sale and purchase of property located in Singapore. BSD will be computed on the purchase price as stated in the document to be stamped or market value of the property (whichever is the higher amount).

If there is a benefit associated with the acquisition, and the benefit is stated in the document to be stamped and is a cash discount (i.e. cash, non-post dated cashier’s order or cheque) to be given to the purchaser upon execution of the document (and not later), the amount of discount may be deducted from the purchase price to determine the consideration for stamp duty purpose. This is provided that the nett price is still reflective of market value.

If the document to be stamped stated a non-cash benefit to be given (e.g. furniture voucher, rental guarantee, car or lucky draw), the value of benefit is not deductible from the purchase price for stamp duty purpose.

If the cash or non- cash benefit is not stated in the document to be stamped, the value of the benefit is also not deductible from the purchase price for stamp duty purpose.

The first instrument executed relating to a sale and purchase is liable to ad valorem duty (i.e. full duty). Subsequent document(s) relating to the same sale transaction are not liable to stamp duty.